Cameron Gleeson

5 minutes reading time

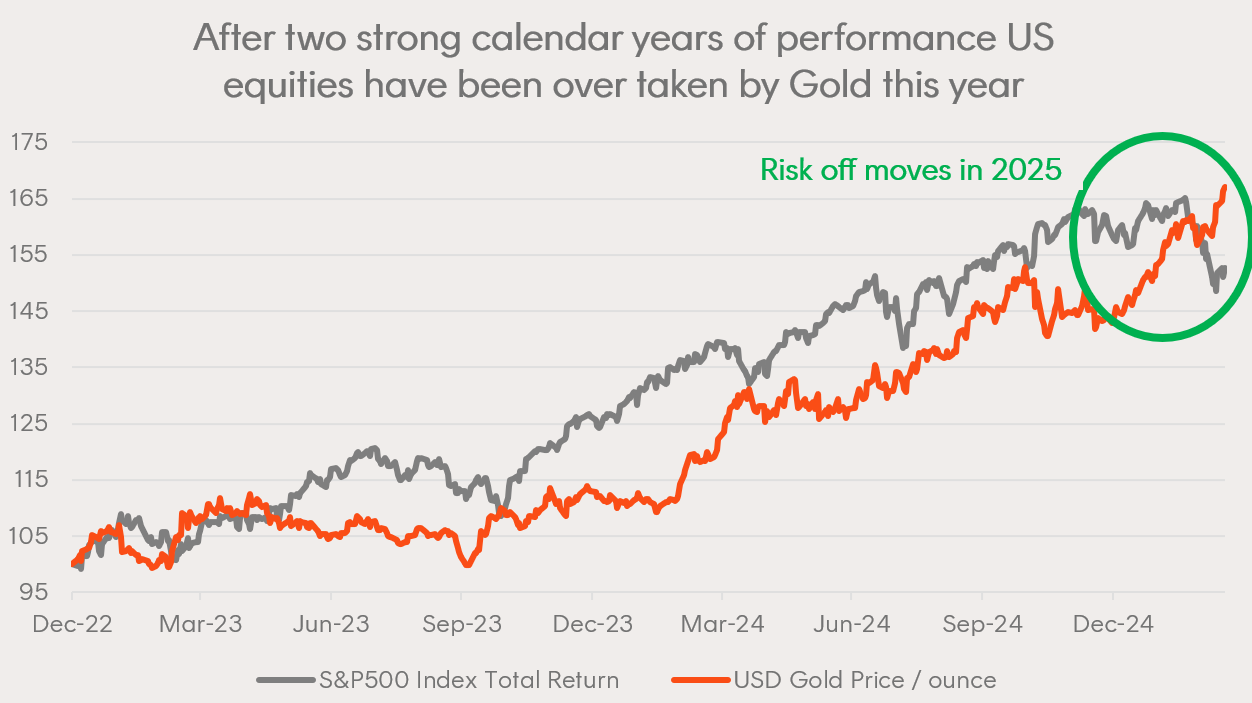

Investor sentiment has turned decidedly bearish in 2025. The initial exuberance at Trump’s election victory has been replaced with fears over policy uncertainty, DOGE cuts, and deteriorating international relations. Last week’s projections of lower growth and higher inflation from the Federal Reserve reflect the mood of the market since the S&P 500 peaked in mid-February.

Put together, it’s little wonder that stocks have fallen, and investors have sought safe havens, driving the gold price higher in 2025.

Risk off moves in 2025

Source: Bloomberg, as at 20 March 2025. Returns shown in USD terms. You cannot invest directly in an index. Past performance is not an indicator of future performance.

However, what some investors may not appreciate is how well gold performed while equities were running hot in 2023 and 2024. This suggests that historically, gold may not be just a rainy day investment. Since the turn of the century, the S&P 500 Index has beaten major European, Japanese and Emerging Market indices (in US dollar terms). But gold has been even more exceptional over that period. An investor with US$10,000 in 31 December 1999 might have turned that figure into US$54,700 today by investing in the S&P 500 Index (assuming dividends were reinvested), or a remarkable US$89,200 had they indeed chosen to buy gold.1

It’s important to recognise that past performance is not an indicator of future performance, and we are not suggesting that investors sell all their equities and switch to holding 100% in gold. But historically gold has demonstrated its ability as a store of value over the long term and the ability to deliver solid returns in a range of environments. Given the twin risks of high inflation and lower growth right now, we believe gold is uniquely positioned for the current risk off environment.

In this piece, we’ll examine the reasons why this trend may continue and unpack the various drivers that matter right now.

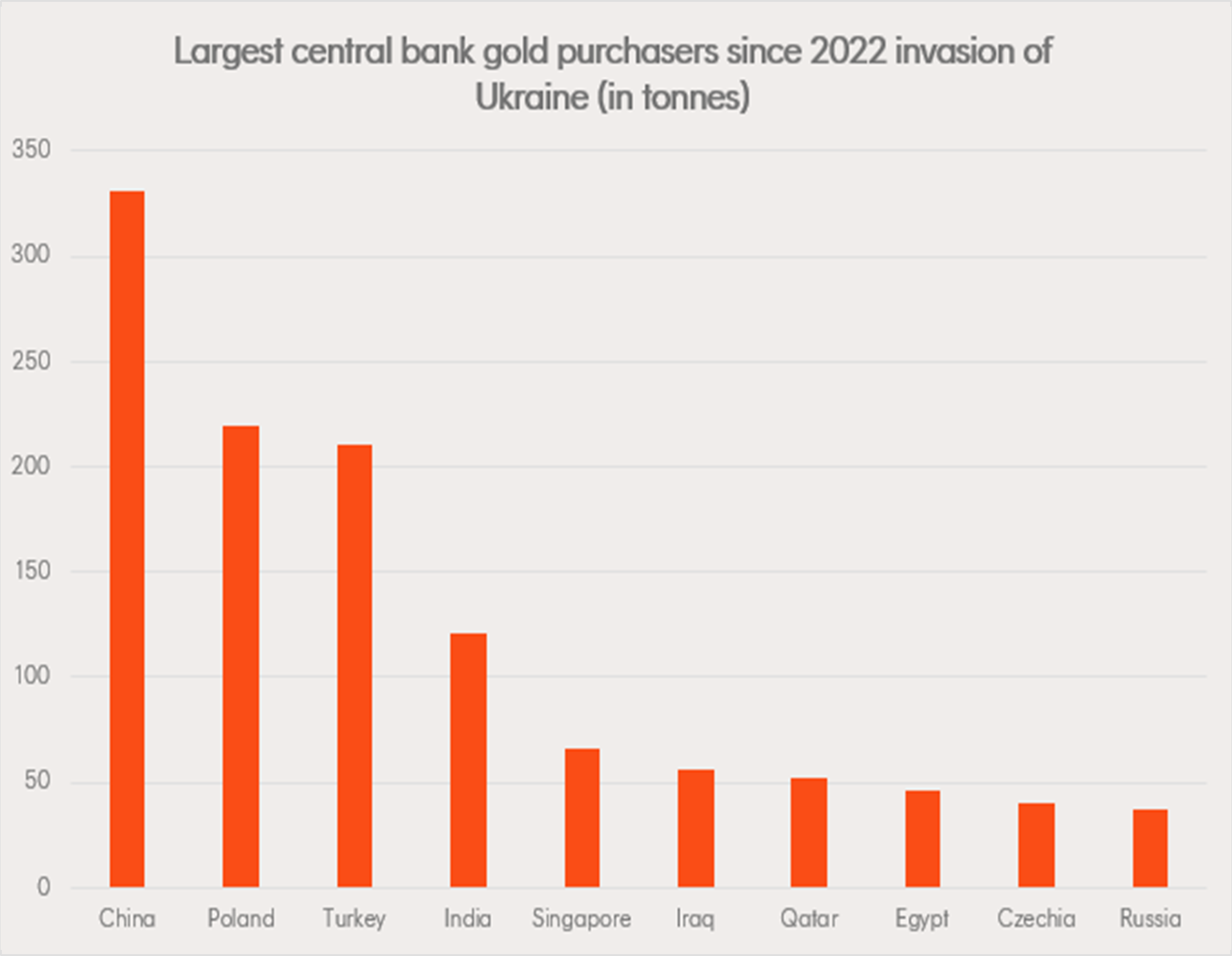

Reason 1: Central banks have been buying

The escalation in geopolitical tensions has caused central banks to buy a lot of gold.

Central banks see gold as a stable way to diversify their reserves beyond foreign currencies like the USD and US Treasuries. In the wake of the Russian invasion of Ukraine, the US showed they were not afraid to ‘weaponise’ the dollar-centric global financial system by imposing crippling sanctions on another nation state.

In response, some non-US aligned central banks have turned to gold. Since February 2022, total reported central bank buying has jumped significantly. Demand has been driven by such countries as China, India, Poland, Turkey and Egypt.

Source: World Gold Council. Net purchases and sales from 1 February 2022 to 31 December 2024.

Reason 2: Cyclical support from consumers and investors

China and India are currently the world’s largest gold markets. With Asia makes up more than 60% of annual demand, the World Gold Council forecasts that consumers and investors from the region may provide significant support for higher gold prices.2 China has seen a boom in demand for gold jewellery with millennials and Gen Z consumers driving this demand.3 In the second half of 2024, Indian demand jumped, thanks to strong economic growth and the reduction of customs duty on gold imports4.

Investors are also buying gold and gold ETFs. Last month, US investors bought US$5 billion in gold-backed ETFs in one week5. In the first two months of 2025, our QAU Gold Bullion Currency Hedged ETF has seen over $60 million in net inflows. This suggests strong investor interest for the yellow metal.

Reason 3: Gold’s main rival as a safe haven is expensive

At the outset, the US dollar surged following Trump’s second election. But those gains have started to fade away because of the potential implications of the administration’s tariff policy on inflation and growth. When investors are questioning whether inflation or growth is the bigger problem, it brings into doubt the US exceptionalism thesis. This concern is starting to weigh on the US dollar and conversely increase gold’s attractiveness as a ‘safe haven’ asset.

Sources: Bloomberg; Citi; Trade weighted real effective exchange rates; as at 18 February 2025

Despite some weakness over the last month, the US dollar remains almost as expensive as it has ever been over the last 30 years, on a purchasing power parity basis. Given this, the US dollar could decline significantly from its current level. Add in the heightened volatility seen in currency markets, and it may not take much for gold to rally even further in US dollar terms.

Other sparks for a gold rally (in US dollar terms) include the possibility of meaningful Chinese stimulus measures announced in the wake of Trump’s heightened trade war and whether America’s fiscal position comes under significant threat.

Hedge your gold exposure

Put together, adding some exposure to the US dollar gold price could be an intelligent move.

QAU Gold Bullion Currency Hedged ETF is physically backed by gold bullion held in a segregated account with a third-party custodian.

QAU is the only currency-hedged gold ETF currently available in the Australian market. This means you will get ‘purer’ exposure to the US dollar gold price rather than the Australian dollar price of gold. With gold breaking through the psychologically important US$3,000/oz level, it may be a good time consider holding this ETF as a satellite allocation to your portfolio.

Footnotes:

1. This simple comparison does not consider the costs involved and is meant for illustrative purposes only. You cannot invest directly in an index. Does not take into account any ETF fees and costs. Past performance is not an indicator of future performance. ↑

2. Source: World Gold Council, Gold Outlook, 2025. ↑

3. Source: Bloomberg, Why Are Chinese Consumers So Keen on Gold? | Big Take Asia, 30 January 2025. ↑

4. https://www.gold.org/goldhub/gold-focus/2025/03/india-gold-market-update-investment-appetite-upheld ↑

5. https://www.reuters.com/business/finance/gold-etfs-drew-largest-weekly-inflow-since-march-2022-says-wgc-2025-02-24/#:~:text=Gold%20ETFs%20saw%20an%20inflow,the%20largest%20since%20August%2C%202023. ↑