David Bassanese

4 minutes reading time

Global markets

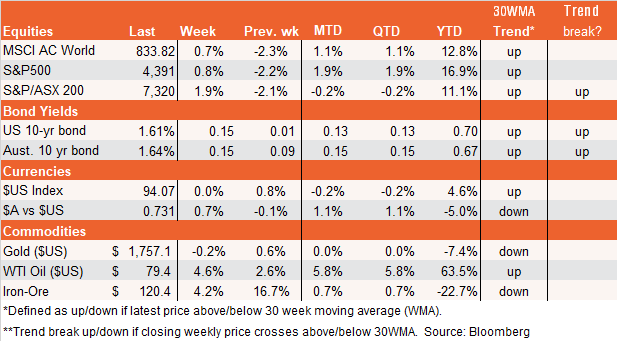

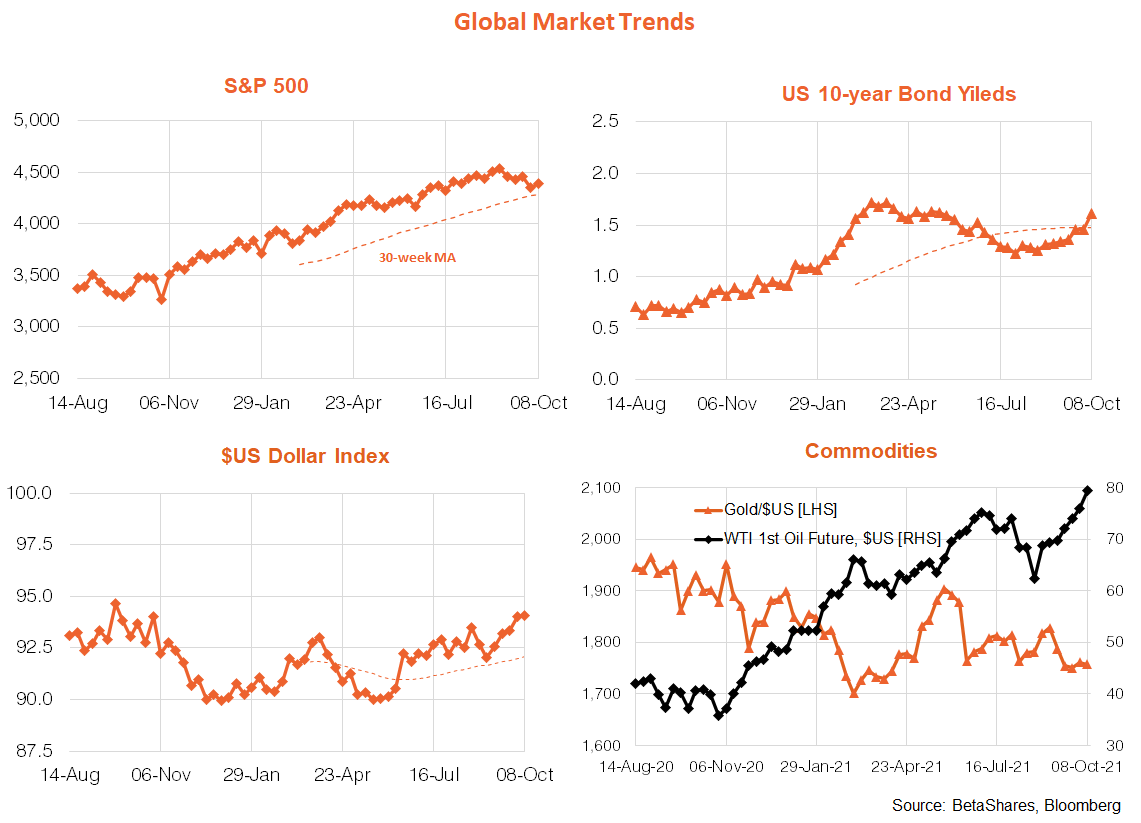

Global equities bounced back last week reflecting an 11th hour deal in Washington to kick the debt ceiling can down the road until early December. Such is the likely short-run oversold nature of equity markets, that was enough for the market to bounce even though most other news last week was hardly reassuring. Most notably, U.S. 10-year bonds bond yields rose a further 0.15pp over the week to 1.61%, while Friday’s weaker than expected U.S. payrolls report highlighted persistent labour shortages and associated wage pressure as the economy re-opens. Further oil price gains and gas supply shortages in Europe add to the ‘stagflation’ narrative.

U.S. employment rose by a much weaker than expected 194k in September, while average hourly earnings rose a stronger than expected 0.6% (4.6% year on year). One factor behind the weak employment result was a smaller than usual seasonal lift in public education jobs, which in turn was blamed on difficulty in finding staff – reflecting lingering fear of COVID, vaccine mandates, and the temporary Federal unemployment benefit supplement (which ended across all states in September). To attract staff, wages in the retail, education and health care sectors have clearly lifted – and the big question in coming months is whether the still low labour force participation rate starts to recover with the vaccine rollout and the end to temporary unemployment benefits.

As regards the Fed, the mixed payrolls result (weaker employment but higher wages) likely means it’s still on track to formally announce bond tapering at the November meeting, though the speed and start date remain unclear (Will they start in December or early next year? How fast will they reduce bond purchases?).

There’ll be more for nervous markets to mull over this week, with minutes to the ‘hawkish’ Fed September meeting on Wednesday, along with the consumer price index. The core CPI (i.e. excluding food and energy) is expected to rise by 0.3%, keeping annual growth steady at 4%. U.S. retail sales and consumer sentiment are released on Friday. The worst case scenario for markets this week would be a higher than expected CPI and weaker than expected consumer sentiment (the latter negatively impacted by rising prices) – which play on the theme of supply-chain ‘stagflation’ disrupting the economy. The Fed minutes, meanwhile, may shed a little more light on the taper start date and timing.

This week also kicks off the Q3 U.S. earnings reporting season, with major bank stocks leading the way as usual. According to FactSet, S&P 500 companies are expected to report earnings around 28% higher than year ago levels. Of the 21 companies (4%) that have already reported, the earnings ‘beat rate’ is broadly in line with its 5-year average. Of most concern this season will be the number of companies citing supply-chain disruption and/or labour shortages as negatively affecting the outlook. Again, according to FactSet, 70% of the (admittedly) small number of companies that have reported so far cite negative supply-chain impacts.

Global equity themes

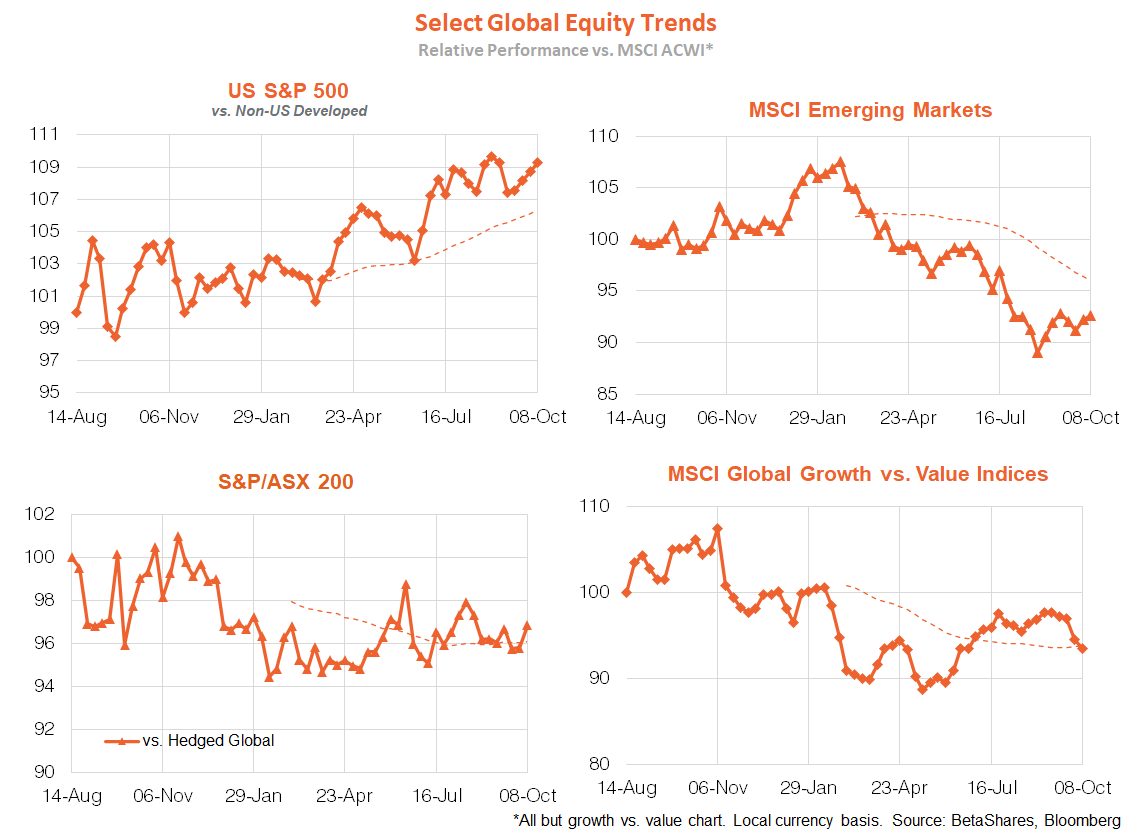

In terms of equity themes, the rebound in bond yields in recent weeks has seen value (such as energy and financials) return to favour over growth (such as technology). The U.S. is still holding up relative to other developed markets, especially given renewed weakness in Japanese stocks. Emerging markets are trying to stage a comeback while relative Australian performance remains choppy.

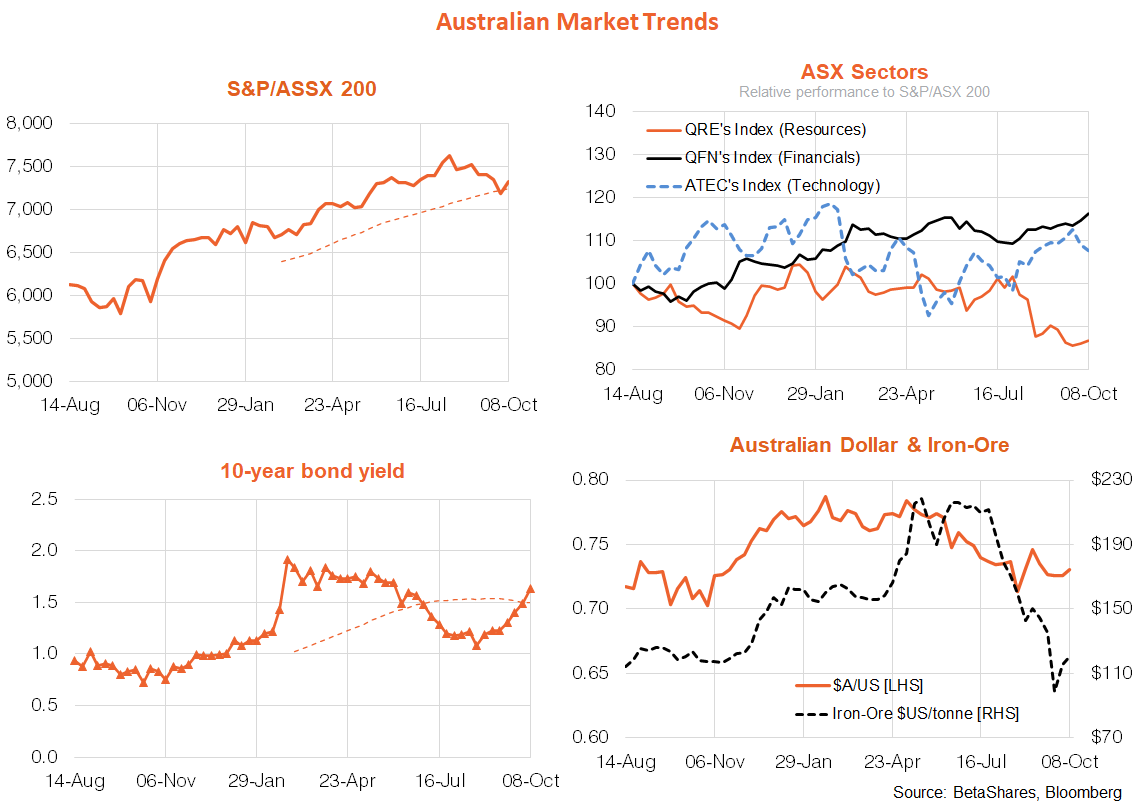

Australian market

Australian equites recovered nicely along with global markets last week, though will need to factor in Friday’s Wall Street decline this morning. The key highlight last week was APRA’s official announcement of renewed macro-prudential controls to keep a lid on house prices, by insisting banks ensure borrowers could service a loan even with mortgage rates 3% above current levels.

Of course, the cruelty of such a sledgehammer approach is that it’s the better-off households that will be least affected, meaning lower income first-home buyers will find it even more difficult to get a toehold in the market. Local 10-year bond yields also rose as much as in the U.S. even though our central banks appears far more dovish.

As for the week ahead, the NAB and Westpac measures of business and consumer sentiment are released on Tuesday and Wednesday respectively, while Thursday’s September labour force report is expected to show a massive 120k slump in employment due to the NSW/Victorian lockdowns. Again, to a large extent this is old news – markets are forward-looking – and with today being ‘Freedom Day’ in NSW, the Australian economy is probably close to bottom right now.

Have a great week!