Liberation Day

David Bassanese

4 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Global markets

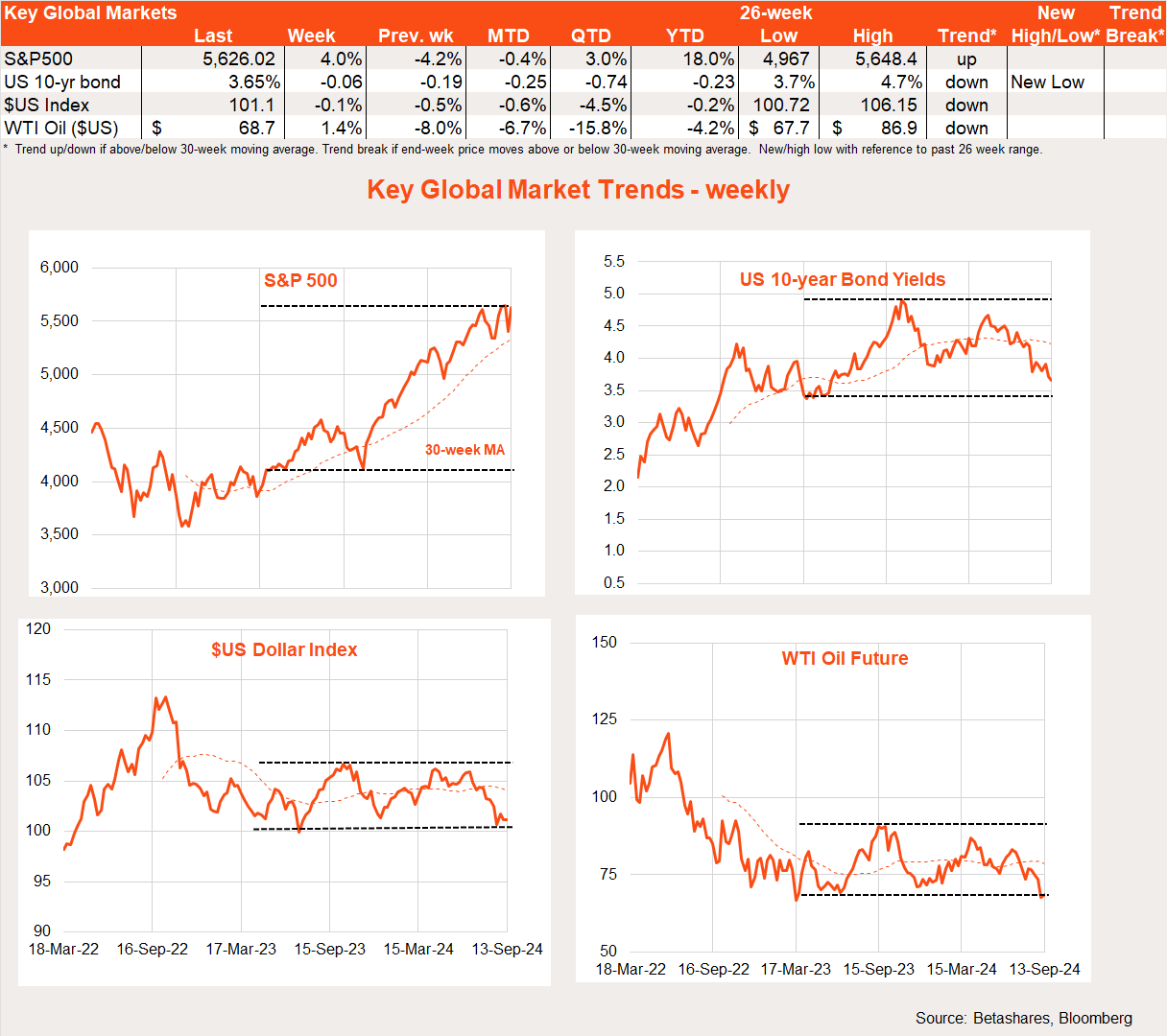

Global equities bounced back solidly last week as benign US economic data heightened expectations for a US rate cut this week.

The US Presidential debate was a non-event for markets. As I’ve argued in the past, markets don’t seem to mind which candidate wins – as each has pluses and negatives as far as financial markets are concerned. So the fact Harris appeared to do well and got a poll boost hardly caused a ripple on Wall Street.

Perhaps more important, US economic data continued to support the ‘soft landing’ scenario, with another reassuringly low weekly jobless claims report and benign consumer price inflation report. Headline consumer prices rose 0.2% in August – in line with expectations. While core prices (i.e. excluding food and energy) rose a touch stronger-than-expected 0.3%, most of this was in shelter costs – which we know should continue to trend down given the already apparent flatness in rents on new leases.

Also supporting markets last week was a widely-expected second rate cut from the European Central Bank.

Global week ahead

The obvious highlight this week will be the Fed meeting over Tuesday and Wednesday (US time). Absent clearer recession signs, markets are expecting only a 0.25% cut – the Fed is unlikely to do more, if only not to scare the horses.

US retail sales on Tuesday will also be of interest – given ongoing concerns over whether the Fed is behind the curve and the economy is tipping into recession.

Policy meetings by the Bank of England and Bank of Japan round out the week. Given market volatility following the BOJ’s surprise rate hike in late July (which triggered the unwinding of yen carry trades) it’s expected to hold off raising rates this week – though further hikes are still expected in coming months. On balance, markets also expect the BOE to hold off cutting rates again this week – consistent with a measured pace of policy easing, given it began to cut rates only last month.

Market trends

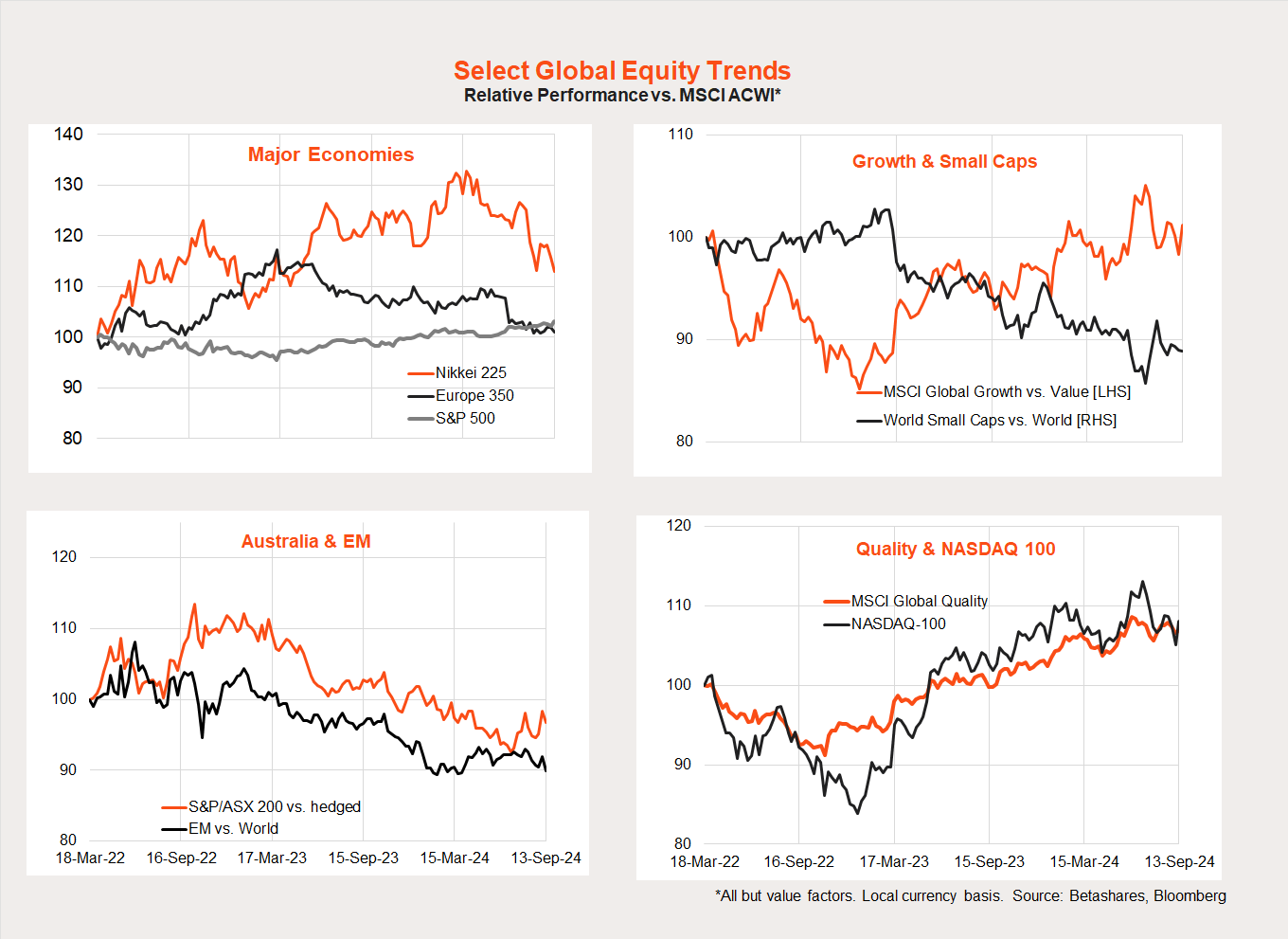

The growth/technology areas enjoyed the strongest bounce backs last week – consistent with view that the ‘great rotation’ towards cheaper parts of the global market so far remains largely directional (i.e. tends mainly to happen in market sell-offs).

All up, we’ll need the dust to settle from recent market volatility to discern whether the much-debated broadening in the global equity rally will gather steam. Can cheaper value stocks outperform as equity markets continue to trend up? I suspect they can, but the evidence to date remains patchy.

Australian market

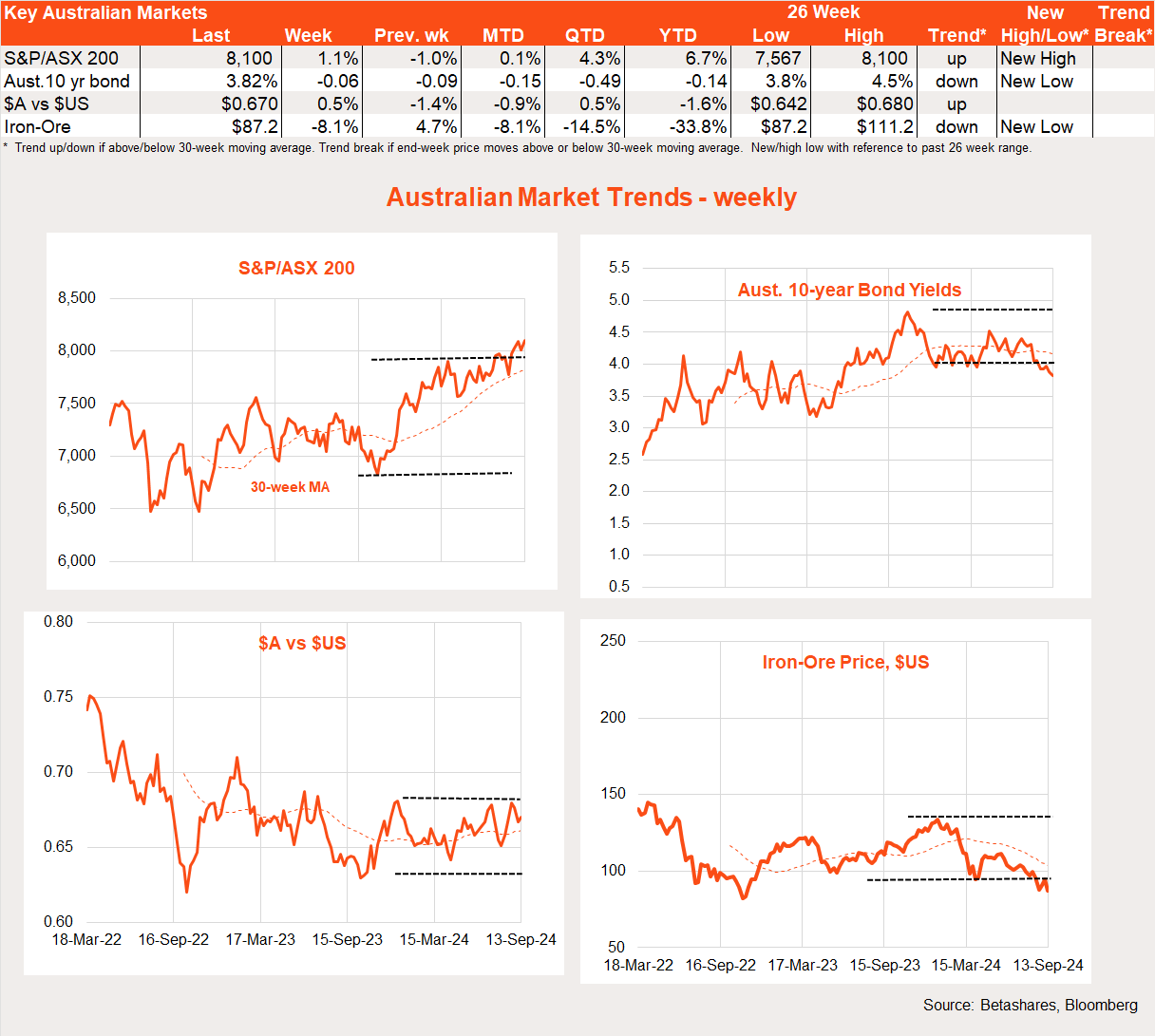

Local stocks bounced back 1.1% last week, with the beaten down materials sector rebounding 5.6% and financials down 0.8%.

Highlights last week were the NAB business and Westpac/Melbourne Institute consumer sentiment reports – which both displayed a further waning in confidence, with fear over interest rates and inflation increasingly giving way to concerns over the weakened state of the economy.

Sadly we’re likely to remain in this funk until the RBA relents and cuts interest rates – which is not likely until we see further convincing signs of easing inflation, which in turn is not likely at least until early 2025.

That said, a rate cut is possible beforehand – but only if we get a more material weakening in the economy. Against this backdrop, the highlight this week is Thursday’s labour market report, with a still reasonable 25k employment gain expected, which should keep the unemployment rate steady at 4.2% – not bad enough to change’s the RBA’s mind on rates anytime soon!

Have a great week!

Explore

Bassanese bites

1 comment on this

Thanks David