Fed meeting recap: hawkish quarter point rate cut

Patrick Poke

8 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Periodically, the world of finance throws up enticing investment trends capable of seducing even the most disciplined investors into changing their strategy.

The beginning of this year exemplifies this phenomenon, as much attention is centred around the unfolding excitement in the US, particularly with Nvidia and the ‘Magnificent Seven’ leading the charge in the AI craze.

This surge has ignited lively discussions across various social media platforms, with investors posing a spectrum of questions ranging from bold inquiries like “Should I go all-in on Nvidia?” to cautious reflections such as “Is it wise to sell everything before a potential market downturn?”.

In this blog, we explore the risks associated with impulsively reacting to investment trends fuelled by media hype, and explain why prudent asset selection, diversification, and maintaining a composed approach are essential for long-term success.

When chasing performance backfires

Over the past 15 years, we’ve observed a wide range of hot trends, including the rise of coal seam gas, the emergence of buy now, pay later platforms, the surge of cryptocurrencies, the cannabis craze, and the heightened interest in healthcare stocks prompted by COVID-19.

While acknowledging the validity of some of these trends, it’s crucial to recognise that exuberance surrounding these investments led to such significant distortions in their fundamentals that it contributed to massive boom-bust cycles. Consider the examples outlined in the table below.

| Company | Theme | Decline from peak price |

| Karoon Gas | Coal seam gas (2009-10) | -82% |

| Cann Group | Medical cannabis (2017-18) | -98% |

| Gamestop | Short squeeze (2021) | -83% |

| Dogecoin | Endorsement by Elon Musk (2021) | -84% |

Source: Betashares (as of February 25, 2024). Peak price denotes the highest value reached by the stock or asset according to publicly accessible data.

Many of these became 10-baggers quickly, only for those gains to evaporate before most investors knew what hit them.

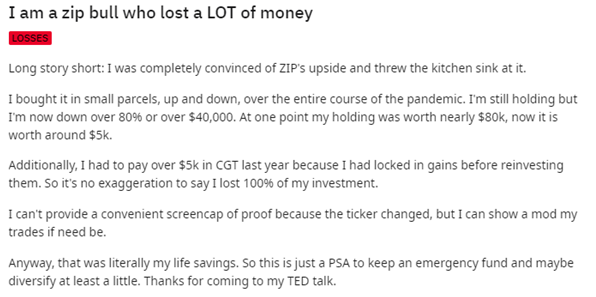

The once lively forums, brimming with excitement over these companies, quickly transformed into realms of despondency. Some investors, like the individual mentioned below, found themselves grappling with a market downturn and steep losses of hard-earned savings.

Source: Reddit.

Yet even disciplined and diversified investors are not immune to the allure of chasing fads, as evidenced by empirical data.

A US study revealed that despite the S&P 500 returning 9.65% p.a. over a 30-year period ending in 2022, the average equity fund investor achieved only a 6.81% annual return during the same time1. This significant variance can be attributed to factors including emotional decision-making, excessive trading activity and incurring high fees.

The pain train: Key lessons for investors

When reflecting on these market bubbles, it’s essential to distill the key lessons for investors:

- The dangers of herd mentality: Investing due to the fear of missing out (FOMO) often leads to poor outcomes. As Warren Buffett once wisely cautioned, “Never invest in a business you cannot understand.”

- Having unrealistic expectations: Assuming that recent high returns will persist indefinitely is a common mistake. Investments don’t go up in a straight line forever.

- Investors often get timing wrong: Unfortunately, investors who chase performance often buy when prices are near their peak and sell at or near the bottom.

- Be mindful of concentration risk: Placing all or sizable portions of your wealth into a single investment can jeopardise your long-term financial security if things go wrong.

- Don’t ignore costs: Frequent trading incurs higher transaction costs, which gradually diminish investment returns over time.

Asset allocation is the ultimate driver of success

While many investors are enticed by the prospect of predicting the market’s next big winner, they shouldn’t overlook the most crucial element of long-term success: asset allocation.

Your asset allocation is probably the most important decision you will make. According to Roger G. Ibbotson and Paul D. Kaplan, asset allocation explains about 90% of the variability of investment returns over time2.

Asset allocation involves distributing your money across various asset classes including shares, bonds, cash, and others. Each asset class carries its own level of risk and potential returns, so diversifying helps mitigate the risk of significant losses from any single investment.

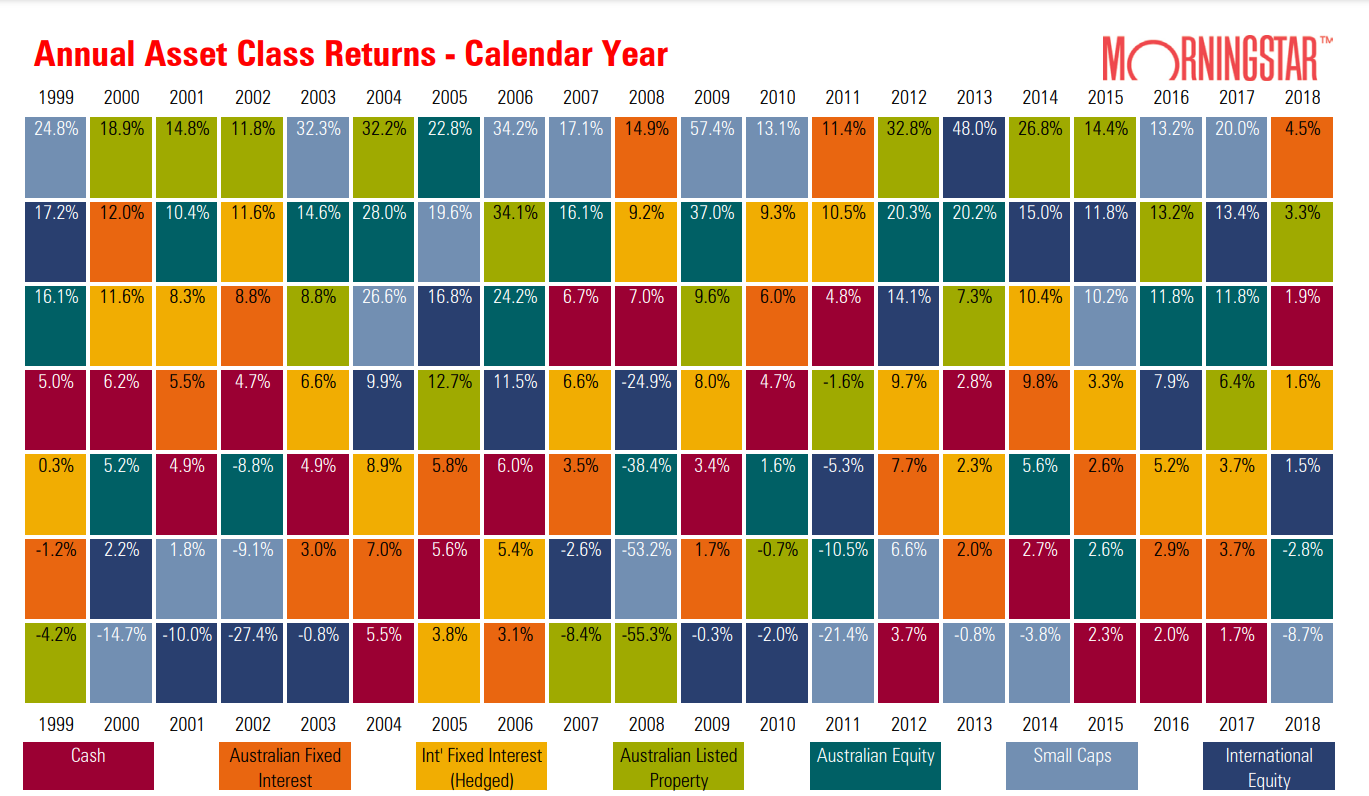

As the data in the table below demonstrates, predicting the top-performing asset class in any given year is challenging3. For example, during periods of poor sharemarket performance such as 2008, 2009 and 2020, bonds acted as a shock absorber, improving overall returns while providing income.

Source: Morningstar. Cash – RBA Bank accepted Bills 90 Days; Aust. Fixed Interest – UBS Composite 0+ Yr TR AUD; Intl. Fixed Interest (H) – BarCap Global Aggregate TR Hdg AUD; A-REITs – S&P/ASX 300 A-REIT TR; Global REITs (H) – UBS Global Investors Ex AUS NR Hdg AUD; Aust. Equity – S&P/ASX 200 TR; Small Caps – S&P/ASX Small Ordinaries TR; Intl. Equity – MSCI World Ex Australia NR AUD © 2018 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs. Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest. Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance.

How to determine the right asset allocation

Finding the right asset mix requires some initial groundwork. We’ve laid out key steps to help you determine it.

1. Understand your goals

Your investment journey starts with a clear understanding of your goals. To define your goals, consider questions such as:

- What are you saving and investing for?

- When will you need access to these funds?

Remember, goals can evolve over time, so periodically reassess how changes to your circumstances may affect your overall strategy.

2. Establish your asset mix

Asset allocation boils down to a simple principle: dividing your investment portfolio into different categories like stocks, bonds, cash and alternatives.

Crafting the right mix and amount invested in each category depends on factors including your age, time horizon, goals and risk tolerance.

3. Determine investment choices

You’ll then want to think about how you’ll put your asset allocation choices into play. There are three main ways to implement this:

- Direct shares: Offer direct ownership of a company but carry stock-specific risks.

- Managed funds: Pool money from multiple investors and invest in a portfolio of assets such as stocks or bonds.

- ETFs: Special managed funds tradable on an exchange like the ASX, offering better liquidity and transparency.

4. Consider costs

Take into account the management expense ratio (MER) and implementation costs (brokerage) associated with each investment, as these costs vary between active and passive investments.

One approach to consider is the core-satellite strategy, where the bulk of your investments are held in low-cost ETFs, while you allocate smaller portions to individual stocks or managed funds.

This way you keep costs low, but retain the flexibility to invest small amounts into assets with higher return potential with manageable concentration risk.

5. Maintain portfolio balance

Rebalancing entails adjusting your portfolio to realign with its target asset allocation.

For instance, if you initially allocated 80% to shares and 20% to bonds, but due to market gains, the share portion increased to 85%, rebalancing would involve selling some shares to return to the desired 80-20 split.

While there isn’t a universal method for rebalancing, experts typically suggest doing so once or twice a year to ensure your portfolio stays aligned with your investment objectives.

ETFs for asset allocation

Some of the ETFs you can use to achieve diversified exposure to different asset classes include:

- A200 Australia 200 ETF : Offering a cost-effective pathway to Australia’s top 200 companies, including industry giants like CommBank, Telstra, CSL, and BHP, this ETF provides instant and diversified exposure to the domestic share market (before fees and expenses), making it a solid portfolio core.

- QNDQ Nasdaq 100 Equal Weight ETF : In response to the surge of interest in certain Nasdaq-listed companies driven by the AI craze, QNDQ adopts an equal-weight approach, limiting each stock to 1% of the portfolio at rebalance. This strategy mitigates overexposure to individual stocks like Nvidia, Microsoft, and Meta, offering investors a well-rounded exposure to the technology sector.

- OZBD Australian Composite Bond ETF : OZBD provides a cost-effective avenue to a diversified portfolio of over 400 quality bonds issued by Australian and state governments, as well as corporates. This ETF serves as a valuable tool for income generation while also offering a cushion against market downturns.

- DHHF Diversified All Growth ETF : DHHF stands out as an all-in-one investment solution, leveraging a passive blend of cost-effective ETFs traded on both the ASX and global exchanges. With exposure to over 8,000 shares listed across 60 exchanges worldwide, DHHF is tailored for investors seeking diversified growth opportunities.

Final thoughts

Determining the appropriate asset allocation and putting your strategy into action may require some time and effort, but building your portfolio itself is relatively straightforward given the tools investors have at their disposal today.

The real challenge lies in maintaining discipline and resisting the urge to constantly adjust your strategy in pursuit of fleeting opportunities in hot stocks, sectors, or markets.

|

Disclaimer There are risks associated with an investment in the Funds, including the specific investment risks noted above. An investment in the Funds should only be made after considering your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Funds, please refer to the relevant Product Disclosure Statement and Target Market Determination, both available on this website. |

References:

1 – https://www.fool.com/the-ascent/buying-stocks/articles/3-reasons-why-the-average-person-actually-stinks-at-investing/2 – Ibbotson, Roger G. and Kaplan, Paul D., Does Asset Allocation Policy Explain 40, 90, 100 Percent Of Performance?3- https://www.morningstar.com.au/insights/markets/237196/how-asset-classes-have-performed-this-year-and-whats-next

Explore

Markets

3 comments on this

An excellent article. It’s so true, and as you say, very experienced investors can still get caught up in such fads. There is not much that will beat index investing over time. Adequate diversification and asset mix are crucial. An index automatically includes winners and throws out losers and one doesn’t have to worry about the performance of any given company.

Just use stop loss or trailing stop loss. hot trend is the best place to make money. This article provides zero insight on how to trade. The market can remain irrational longer than you can remain solvent.

Also stop suggesting people to buy AU200. Its performance is terrible compared to S&P500

Great article. I was tempted to go big on Nvidia but this blog knocked the sense into me to not chase performance, like trader suggests. FYI mate, a stop loss isn’t going to bail you out of a stock dropping 20% in one day. A200 is a portfolio bulwark and it gives me the income I need to enjoy my lifestyle, global shares are for growth, cash is for stability and emergency. You need all of them.